This post is long overdue.

I talk about Bitcoin a lot. In any given week, I’ll have dozens of conversations about bitcoin with various people across different sectors. And like a pendulum oscillating every other year, the narrative of bitcoin not being a medium of exchange keeps coming back. I get it. When influencers from the community are pushing this narrative, people listen. They’re influencers.

But in this post, I want to set the record straight: Bitcoin IS a medium of exchange, now and in the future. What’s more, its future as a store of value (SoV) depends on its acceptance as a medium of exchange (MoE). Some of the people pushing the (false) dichotomy between bitcoin as a SoV and a MoE are doing it for their own self-interest. Some are just hangers-on.

Luckily, these people do not control how bitcoin will continue to develop and be developed. Bitcoin’s future depends on our collective swarm intelligence, and together we’re pretty smart. Here’s the conclusion we will eventually, inevitably reach: the dichotomy of bitcoin is no dichotomy at all. Bitcoin’s durability and deflationary properties are what make it a good SoV. Its divisibility, portability, relative fungibility — along with its decentralization and censorship-resistance — are what make bitcoin a good MoE. But these qualities presuppose each other. Indeed, you can’t have a SoV without a MoE.

There Is No Value Without Exchange

Before determining how the categories of SoV and MoE fit together, we should establish what those terms mean in the first place. While there are conceptual differences between them, neither is really thinkable without the other. There is no SoV without a MoE and vice versa.

SoVs Trade Across Time

Stores of value need to be durable, and they need to retain their value. So far, so obvious. But what does it mean to “retain value”? How could you tell?

There are several ideas about how best to think about value. Marx famously reduced value to labor, so the more labor was invested in producing a thing, the more it would be worth. But this just begs the question: what’s a unit of labor worth? And is a wild strawberry worth less than a cultivated one, even if it’s more delicious?

Then there’s “intrinsic” or “objective” value. In finance, intrinsic value means something like the “true” or “objective” value of an asset as distinguished from its market price, which is supposedly distorted by all the market participants and their (mis)perceptions. A company with plenty of quality machines and a positive bank balance would seem to have value even if its shares were worthless. In strict semantics, intrinsic value would mean that the value is inherent, in the essence of the thing.

But all value is contextual. In the middle of the desert, a barrel of water is worth more than all the gold in the world. The fastest mining rig ever devised is worth nothing to a sadhu. Family heirlooms like your late grandma’s favorite earrings are worth incalculably more to members of that family than to anyone else. You won’t find their value in their objective characteristics.

That’s why many economists and mainstream bitcoiners subscribe to the subjective theory of value. The idea is that there is no value in a transactional vacuum. Value emerges from how people deal with a thing, what they’re willing to trade for it. At some point, aggregate supply will meet aggregate demand – the price – and that’s where the trades will happen.

A price is just the value of one thing expressed in a quantity of something else. A Tag Heuer Connected Calibre E4 trades for $1450 USD, which is equivalent to about 0.02 btc, which is equivalent to …

That’s the first important conceptual point about SoVs: unless they are exchanged sometime, they have no real value. They might have notional value, like the value of an imaginary pet dragon, but their real value would never have the chance to emerge.

The second point is that all SoVs imply a trade by definition; it’s just that the trade is diachronic. In other words, the trade with a SoV is in the same asset at two points in time. Trade a smaller value of thing A in the present for a larger value of thing A in the future. Same asset, two different times.

While we’re thinking about time, consider this: what does it mean for a SoV to appreciate? Its value must be measured relative to something else. In other words, appreciation simply means that its future real price will exceed its current real price; I’ll be able to exchange less of it for more stuff in the future than I can today. Without a trade — even just an unrealized future trade — there is no value.

MoEs Trade Across Assets

MoEs need to be divisible, portable, and fungible. Here the trade is synchronic (at the same time) across different assets rather across time (diachronic) with the same asset. But if MoEs are traded in the present by definition, how short is the present? What’s worth more: owning all the bitcoin that’s ever been mined, but only for one femtosecond, or ten million durable sats?

Some amount of value retention and durability is necessary for a MoE to work. For example, cigarettes are used as currency in prison. But cigarettes go stale after a few weeks, so they don’t retain value very well over time. Those who have them are looking to spend them quickly. Ditto shitcoins whose value might collapse next week. You need to take the trade or reject it now.

Indeed, durability is one of the characteristics that make gold a better MoE than, say, sodium. Gold resists almost any kind of corrosion, so our descendants will still have the same amount of gold to trade generations from now, whereas sodium can’t even get wet without exploding.

So even though conceptually MoEs are exchanged instantaneously in the present, practically speaking they exist in a temporal world of people with finite lifespans, short vacations, and long hours in waiting rooms. A MoE that retains its value is worth more than a perishable MoE, other things being equal. (Interesting wrinkle: when perishability increases scarcity, but let’s not digress.)

And MoEs reinforce the subjective theory of value. If no one wants to buy your artisanal pumpkin spice pasta for the price you’re asking, can you say that everyone is wrong? That no one recognizes its intrinsic value or the value of the hours you’ve invested in making it? Of course not. That monstrosity is worth what people are willing to exchange for it, nothing more and nothing less. Without a subjective, contextual theory of value, it’s hard to conceptualize a MoE in the first place.

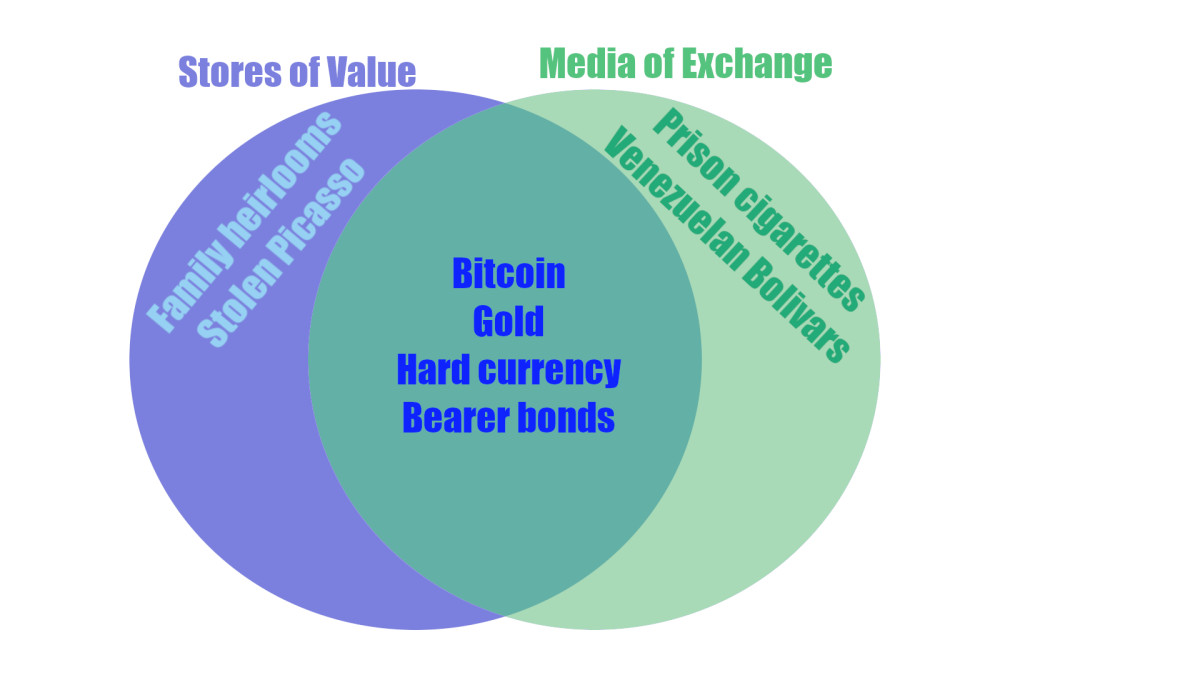

SoV-MoE Convergence

So there are a few edge cases on each side, where the properties of the asset recommend it as either a SoV or a MoE. The harder an asset is to trade, the more it would seem like a SoV. The quicker an asset degrades, the more it would seem like a MoE, up to a point. Without some tradability, a SoV is worthless and no longer a SoV. Without some durability, a MoE is worthless and no longer a MoE. But some assets fall more on one side or the other.

The middle, however, is far from empty. That’s where you’ll find the really good stuff, like gold, bearer bonds, hard currency, and bitcoin of course. What makes them great is that they share the attributes of both SoVs and MoEs. These assets are more or less fungible, portable, and divisible, just like good MoEs. And their value is durable, just like good SoVs.

If people trade them at high velocity, they look more like MoEs. If trades occur at longer intervals, then they look more like SoVs. The substance is the same; it’s the context and the activity that changes how we see them.

Contrast this happy coincidence with the claim of dichotomy. That is, what is bitcoin as a SoV exclusively, i.e. without working as a MoE? Rather than recognize and realize bitcoin’s potential, the SoV-only hypothesis absolves it from ever having to trade. But since value emerges from transactions, never in a vacuum, a SoV that never functions as a MoE has no detectable value.

The idea that bitcoin is only a SoV is not even wrong. It’s incoherent. It’s asserting that bitcoin is a store of value while removing it from the only kinds of context that could allow us to determine its value. SoV and MoE are logically and practically inseparable. A SoV is a MoE in transactional slow motion, and a MoE is a SoV with the trading velocity cranked up.

But enough theory. This is the way things have always been, or at least as far back as archaeology lets us see. We’ll return to bitcoin in a minute, but let’s look at its family tree first. The coincidence of SoVs and MoEs is an empirical reality that goes back millennia.

Storing and Trading Assets Through History

Beyond theory, history provides evidence for the convergence of SoVs and MoEs. History contains a host of assets that function as both MoEs and SoVs because if they’re in demand, you can trade them, and if you can trade them, then it’s good to have a stockpile in storage. SoV and MoE are – and always have been — two sides of the same, er, coin.

Bronze Ingots

The overlap between SoVs and MoEs is illustrated beautifully by Bronze Age oxhide ingots. These ingots were shaped like oxhides, came in roughly standardized weights (usually around 30 kg / 66 lbs.), contained relatively pure copper or tin, and were passed around all around the Mediterranean and beyond from the second millennium BCE — the Bronze Age.

Since everybody was using bronze, copper and tin – the two ingredients of bronze – held their value very well. Everybody could use them. Demand was high and stable. They were also relatively easy to store.

But they were also relatively easy to transport. A load of ingots found in a shipwreck from 1327 BCE contained metal that originated in Uzbekistan, Turkey, Sardinia and Cornwall. Chariots were still relatively new tech, but these hunks of metal were traversing the known world, farther than virtually any human would have traveled, because they were “connected to systems of international distribution, exchange and trade.”

Now let’s say that you’re a Bronze-Age fisherman who comes across a sunken cargo of ingots. Are they a SoV or a MoE? Well, if you’ve had a good season, you might be feeling flush, so you save them for a rainy day, in which case they’re a SoV. If, on the other hand, the fish haven’t been biting and you need some liquidity, then you’d probably trade them quickly, in which case they’re a MoE. But how would you know they were worth saving if they weren’t being traded somewhere to reveal their value? And who could you trade with if there weren’t counterparties out there convinced that owning some ingots around would be a wise financial decision?

The oxhide ingots’ durable, high-demand materials made them good SoVs, and their standardized sizes and portability made them good MoEs. The ingots were both simultaneously because each use implies the other.

Gold

Humans started collecting gold a few millennia before they were into bronze. But at first, gold was principally used for decorative and sacred purposes, like statues and ceremonial jewelry. Since such objects aren’t fungible, they were poor MoEs, and trades were very infrequent. The low trading velocity was due to the impossibility of finding a price: ceremonial objects’ owners would always value them more highly than any counterparty.

Standardized gold coins only started showing up around the 7th century BCE, about 1000 years after the ingots. Interestingly, they appeared in China and Anatolia around the same time. As coins, gold had finally become fungible, which increased the trading velocity and brought the SoV and MoE uses closer together. Coins also offered some advantages over oxhide ingots: a coin doesn’t weigh 30 kg, gold doesn’t corrode, and it didn’t have a lot of other uses, so the supply didn’t have to compete with demand for useful stuff like ploughs and swords made of bronze.

Gold coins were so effective as both a SoV and a MoE that basically everyone started using them, like the Roman aureus, the Almoravid dinar, the Spanish doubloon, the Tokugawa Koban, etc. Even now, 2600 years later, countries from Armenia to Tuvalu are minting and circulating gold coins for people to keep and trade, to store and exchange.

Again, the use of gold coins as a MoE made gold a more obvious and widespread SoV, and their widespread recognition as a SoV made them a more liquid MoE.

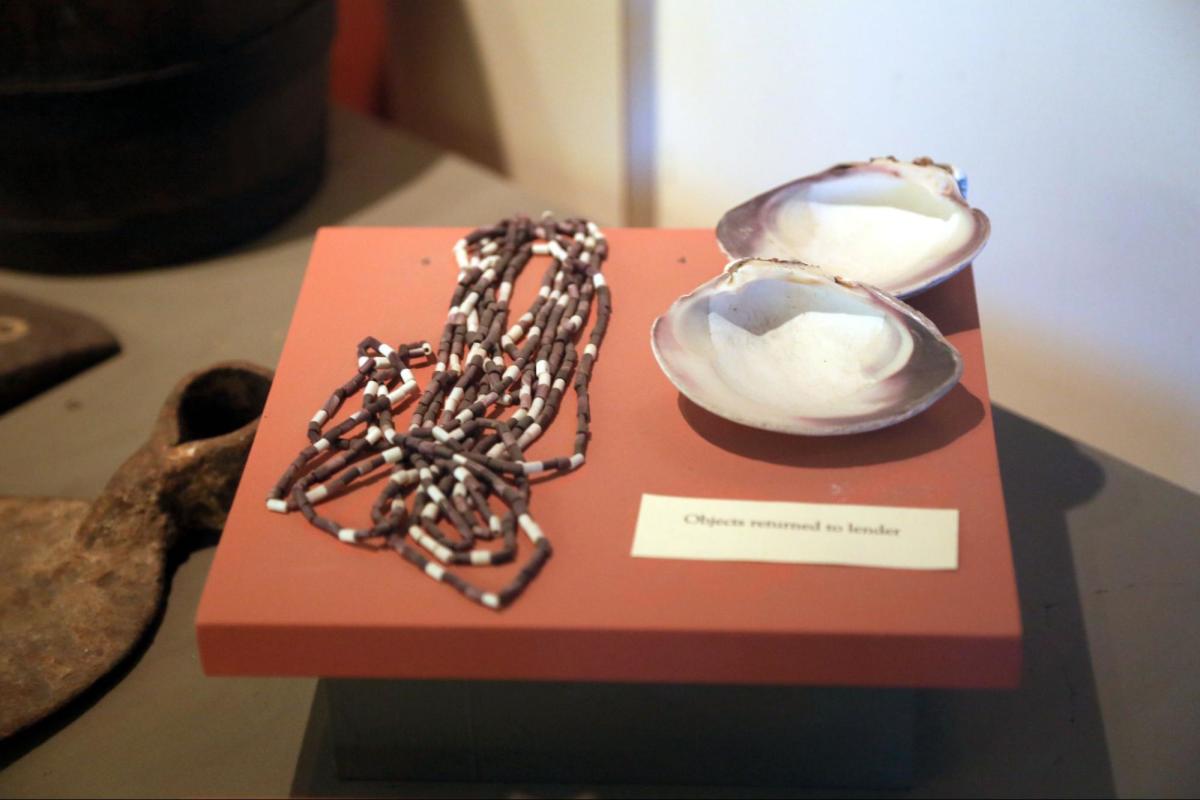

Wampum

In the 17th century, early European settlers on the Atlantic coast of North America and the indigenous peoples of the continent were getting to know each other. The worlds they knew were radically different. No common language, no common religion, no common history, radically different technology, radically different cosmologies. But as humans do, they started to trade pretty quickly. Without commonly recognized SoV-MoEs, though, trading is hard.

At first, fur pelts had a certain value, but they’re bulky, their value was not standardized, they can degrade, etc. They were better than nothing as a SoV and MoE, but not ideal as either. Venetian glass beads also worked, but getting beads from Venice to the European colonies in the “New World” could take months, maybe years.

Then in 1622 a Dutch trader named Jacques Elekens took a Pequot sachem (like a chieftain) hostage and demanded ransom. The sachem’s people brought Elekens 280 yards (~256 m) of white and purple beads made from clam shells – wampum. Apparently, they hadn’t really used wampum as cash before, and even in this instance the ransom had primarily symbolic value, like ransoming a prince by sending a fancy ceremonial scepter.

But Elekens was a trader, and though he missed the transcendent symbolic value of wampum, he saw its profane cash value immediately. If you can buy a chief’s freedom with wampum, what couldn’t you buy? Soon the Europeans were forcing a couple of tribes to produce wampum, and it was traded in units of length, like so-and-so many pelts for so-and-so many fathoms (1 fathom ~ 1.8 m / 6 ft.) of wampum beads.

Wampum quickly became an official MoE. Several colonies adopted wampum beads in standardized values as legal tender, a practice that continued for about a century. And wampum was naturally attractive as a SoV: “the European colonists quickly began trying to amass large quantities of this currency, and shifting control of this currency determined which power would have control of the European-Indigenous trade.” They weren’t just trading with it; they were building currency reserves. They were storing the MoE for its future value, and its future value made it an effective asset to trade today.

The words “gold” and “wampum” still mean money in certain contexts. Speaking of money…

The USD

The power to create money is enshrined in the US Constitution, and the Coinage Act of 1792 pegged the value of the new dollar to the Spanish silver dollar and a fixed quantity of 416 grains of silver. “Eagles” were effectively $10 coins that were to contain 270 grains of gold.

The architects of the dollar were leveraging the historical context that everyone already understood: precious metals work as both MoEs and SoVs. After three and a half millennia, word had got around.

As tends to happen with specie, the coins were debased over time, which means that the minters kept gradually lowering the amount of precious metals contained in the coins. That’s how inflation works with a MoE that’s pegged to keep its value as a SoV. You can still mint the same amount at less cost by manipulating the peg.

The Gold Standard Act of 1900 hardened the peg by making each dollar redeemable for a fixed amount of 25.8 grains of 90% pure gold. So if dollar notes were redeemable for gold, would that make them a MoE or a SoV? The notes circulated, but the US government was committed to storing an equivalent amount of gold to maintain their value. The gold might look like a SoV, and the notes might look like a MoE, but they were equivalent, so it’s only the use that differs, not any deeper nature.

When the Great Depression struck, there was a run on the Federal Reserve. People were concerned about the dollar’s continued viability as a MoE, so they started to redeem their dollars for gold. When the Federal Reserve became concerned about its own ability to continue converting dollars for gold, President Roosevelt suspended the gold standard.

But, of course, bank deposits didn’t fall to zero, so the dollar continued to function as a SoV and MoE. And people were hoarding gold so they could trade it just in case the dollar did lose its utility as a SoV and MoE. But both dollars and gold retained both functions.

The gold standard returned with the Bretton Woods system after the Second World War, but this time the USD was pegged at $35 per ounce of gold, and central banks around the world could exchange their dollars for gold at that rate. This effectively made the USD the hardest currency, and through fixed exchange rates it was supposed to bolster other currencies too. As before, the equivalence through redemption virtually erases any practical distinction between the SoV and the MoE.

For a range of complicated reasons that can be reductively simplified down to “inflationary pressure” (i.e. fiat’s own perverse version of “numbers go up”), the USA had to abandon the international gold standard of Bretton Woods in 1971.

While this was an important turning point for economic historians, the USD remains both a SoV and a MoE. According to the IMF, about 60% of global foreign exchange reserves are held in USD, about 3x as much as the nearest competitor. Other countries store USD just in case they need to exchange it for their own currency to prop up their own currency’s value or to buy necessities in a pinch.

Even without gold backing, demand for USD is astounding. Foreign countries hold $8.8 trillion of American debt — IOUs to be paid in dollars at some point in the future, which looks like a classic SoV. And most international trade is billed and settled in USD. Even in Europe, a continent with its own common currency, over 20% of trade is settled in dollars.

The remarkably resilient demand for greenbacks gives the USA as their minter a privileged position. The phenomenon of “petrodollars” illustrates just how the USD has remained dominant since the collapse of the gold standard. Petroleum exporters sell oil for USD, and they rapidly accumulate large reserves of dollars. They need to spend these dollars, and it just so happens that the US is always eager to sell T-Bills (American I.O.U.s) for dollars to finance its $35 trillion in debt.

As long as other countries hold that debt, they have an interest in preserving the value of the dollar. As long as the dollar can retain its value, it remains useful for trade. As long as it remains useful for trade, other countries will accumulate dollars and dollar-denominated debt. Sound like a Ponzi scheme? Well, it’s not not a Ponzi scheme.

In short, other countries’ foreign reserves of USD let the US trade on a multiple. Hold that thought.

Yes, Bitcoin Is a SoV Is a MoE

Bitcoin is the latest descendant in this lineage of readily tradable SoVs, i.e. of MoEs that people like to hoard because they hold their value. However, there is a widespread, often repeated claim that bitcoin is just a SoV. Indeed, that’s why I’m writing this, and that’s why I feel the burden of proof is on me to demonstrate bitcoin’s viability as a MoE. So far I’ve laid out some theoretical ideas about how SoVs and MoEs are conceptually inseparable and covered several historical examples to demonstrate that this mutual presupposition is how things have worked as far back as history can go. So now let’s turn to bitcoin, which is just new tech following established patterns: MoE and SoV go together because they must.

Transactions in the Trillions

We know bitcoin works as a MoE because people move bitcoin – A LOT. Adjusting for change addresses, River estimates that $14.9T of payments were settled with bitcoin in 2022. So even if 74% of bitcoins don’t move within six months, bitcoin equivalent to the combined GDPs of Germany, Japan, India, and Canada can change hands in just a year.

Trading Bitcoin

There are about 2.35 million btc in exchange accounts (about $150B). This should be puzzling because autonomy and self-custody are two of bitcoin’s major selling points. If bitcoin is just a SoV, why would anyone entrust it to another party rather than keeping it in cold storage themselves? If it’s a store of value, why wouldn’t you store it as safely as possible, especially considering that decently safe storage can cost as little as a piece of paper?

The reason more than one in ten of all bitcoins in existence are held in exchange accounts is to facilitate trading. Exchanges are just that: where people go to trade one asset for another. Bitcoin works beautifully as a MoE for such trades because no other cryptocurrency even comes close to the demand for bitcoin. Whether you go by market cap or unit price, bitcoin is in a league of its own. The only other coin that can compete on any interesting metric is USDT, whose trading volume is roughly double bitcoin’s impressive $26 billion/day. And that is probably because Tether profits from the waning dominance of the legacy global MoE – the USD.

If bitcoin were only a SoV, nobody would leave their hoard on an exchange, and the trading velocity would be miniscule. But they do. And it isn’t.

Merchants Accept Bitcoin

Some might object that, while bitcoin might be a MoE among the tech boys of the financial cognoscenti, it hasn’t penetrated the “real economy” the way a “real” MoE should. But examples of bitcoin circulating in the real economy would be enough to refute this claim. We’re in luck.

Retailers are using bitcoin as a MoE because it already offers concrete benefits. Take one brilliant example from the recent River report: Atoms, a Brooklyn shoe company. In 2021, Atoms started accepting bitcoin as payment and launched a bitcoin-themed sneaker. Atoms accepts bitcoin as a MoE (consumers pay for shoes with bitcoins), and then Atoms hold it as a SoV until the need arises. And when it does, their SoV bitcoin is automatically tradable MoE bitcoin because it’s the same bitcoin.

Atoms proves that the dichotomy is strictly conceptual and misguided. Actual bitcoin is both a SoV and a MoE; it just depends on how its owner happens to be using it at the moment.

And Atoms is not alone, not by a long shot. Balenciaga accepts bitcoin. Tag Heuer accepts bitcoin. AMC Theatres, PayPal, twitch, Ferrari, and Proton all accept bitcoin. Is anybody going to claim that AMC or PayPal are niche vendors known only to nerds with obscure financial hobbies?

Are these famous, global brands hodling bitcoin as a SoV or trading it as a MoE? There’s that dichotomous thinking again. Bitcoin is a divisible, fungible, durable asset, so they can hold it as long as they want and trade it at any time. They can accept it, spend it, lend it, whatever. Bitcoin has no fundamental essence. It is whatever they/we use it for.

All MoEs and SoVs Are Just Betas

Another major lesson from the examples above is that SoVs and MoEs never stop evolving. Bronze Age fintech was about standardizing ingots and purifying the metals they contained (or, for the ruling class, maybe debasing them). How SoV-MoEs are designed affects how we use them, which influences their design, which affects how we use them, and so on. But evolution is always about local optimization, never perfection, so there will always be room for further improvement.

Good money has always served as both a SoV and a MoE, and bitcoin still has room to grow. Let’s consider the areas where bitcoin could use further optimization.

Fiat’s First-Mover Advantage

If asked, virtually every friend of bitcoin would prefer to receive their income in btc while paying their expenses in fiat. But this doesn’t mean that bitcoin is defective as a MoE; it means that fiat is defective as a SoV. People prefer to hold bitcoin because bitcoin holds its value better than fiat, so it makes sense to save the bitcoin for tomorrow when it will be worth more and spend the fiat today before it’s worth less.

So fiat’s edge is just that it has built up 13 centuries of network effects to compensate for its obvious defects. People know fiat. The world’s payroll systems, tax codes, and banking systems are built around fiat. The world has considerable sunk costs in the fiat project. That’s why it’s so important for bitcoin to exceed fiat in any metric: value retention, autonomy, censorship resistance, and of course…

The UX. Always the UX.

Bitcoin’s UX is improving. Many innovations are unequivocally ameliorations. The Lightning Network, for example, increases bitcoin’s maximum trading velocity by multiple orders of magnitude.

Other aspects of using bitcoin, however, can be features and bugs simultaneously. The most obvious is self-custody. Holding your own bitcoin is really the only way to fully enjoy the autonomy and freedom bitcoin affords, whether as a SoV or a MoE or both. But with great power comes great responsibility, and assessing and implementing different ways to store and use bitcoin can be a bit much for many no-coiners.

And even for all its benefits, Lightning has limitations that we’re still trying to overcome. Lightning adds complexity to liquidity management, although LSPs are helping to transform liquidity from a difficult technical problem into a largely automated financial consideration. But friction is friction.

Similarly, Lightning can only take on new users so fast because each new user requires at least one on-chain transaction and additional liquidity. New technology, like Breez’s nodeless SDK implementation, can improve Lightning’s throughput and mitigate its liquidity constraints just like Lightning surpasses on-chain bitcoin for some use cases.

And if this trend of innovation → UX tweaking → innovation continues as it has for fiat, we’re in good shape. Consider the credit card. Nobody used credit cards for small purchases for the first three decades or so of their existence. It was a big story when Burger King started accepting credit cards in 1993. People even got all judgmental about it. “I think it’s pretty bad if you have to use a credit card when you go to a fast food restaurant.” Credit cards were for big purchases, like airfare, jewelry, hotel stays, and car repairs. In 2024, about a third of payments are made by credit card, and nobody – not a single living soul — cares if you pay for an order of fries or bus fare with a credit card.

People in 1993 react to #creditcards being accepted at a #burgerking

As credit cards became easier to use (it used to be hard work), people used them more and for smaller purchases. The lesson here is that people will use an asset as a MoE selectively if the UX is rocky, using it more frequently and for smaller purchases as the UX improves.

Legal/Regulatory Treatment

We’ve all heard the outdated FUD that bitcoin is basically just for criminals. Proton is a great company that accepts bitcoin and is advised by Sir Tim Berners Lee — not exactly your typical moustache-twirling supervillain. But people fear what they don’t understand, and legislators and regulators love pandering to popular fears.

Some jurisdictions are open and progressive. In the EU, for example, bitcoin is considered a currency and is treated accordingly in most laws. Exchanging bitcoin for another currency incurs no VAT, but buying a product or service with bitcoin does incur VAT, just as it would with any other currency.

In the US, while some regulators and courts have acknowledged that bitcoin is “a medium of exchange and a means of payment,” the IRS treats it as a property subject to capital gains tax, which makes trading it more expensive and, consequently, slows its trading velocity. So it’s natural that bitcoin might look more like a SoV than a MoE to Americans subject to that tax regime.

Some countries like Morocco and China have banned bitcoin outright. Whatever. King Canute tried to stop the tides until his feet got wet, at which point he declared that no king could gainsay eternal laws. That’s a good lesson for the SoV crowd and the staunch bitcoin opponents alike. People want to be free, and they want their money to be free. If you don’t give it to them, they’ll take it eventually.

Volatility

Many people might be averse to using bitcoin as a MoE because of its characteristics as a SoV. First, its price is relatively volatile. In the last few years, we’ve seen the value of bitcoin relative to the USD swing up and down by a factor of 4x. This makes it hard for consumers to spend and hard for retailers to accept because the exchange rate of bitcoin relative to a given good — i.e. its price — can be too uncertain.

The more disposable income and wealth someone has, the less sensitive they are to volatility. If you still have plenty of income left over every month after taxes, groceries, and mortgage payments along with healthy savings, it won’t matter much if one tranche of your portfolio drops a bit for a few months. You use your assets on a different timescale than price volatility. Long-term gains more than outweigh short-term drops, so let it swing.

Many others are not so privileged. Their income is their wealth; they have no savings or surplus to buffer price swings. For them, a sudden drop in the value of their income could mean hungry days at the end of the month. If they obtain bitcoin (and many do), they’re likely to exchange it for a more stable asset as soon as they can.

Bitcoin’s volatility is a boon to some, a curse to others, and irrelevant to many. We can, however, see a natural path forward for it to appeal to all user groups. One way to think about bitcoin’s volatility is as a woefully incomplete index. The value of fiat is usually measured by exchange rates to other currencies, by official “baskets” of goods to determine its official purchasing power parity/consumer price index, and by millions of people just transacting in their everyday lives. Each source of information provides a check on the others, triangulating something like a “true market value.” The more people transact and the more goods are priced in bitcoin, the more precise the triangulation, and the less need for price swings.

In other words, the more people use bitcoin as a MoE, the more its price curve will stabilize relative to other assets. Even as a speculative asset, it would look more like T-Bills than, say, oil. And vibrant use as a MoE will maintain expectations of its future demand, which, along with its deflationary design, preserves bitcoin’s status as an unprecedented SoV. Greater usage just smoothes the upward curve.

Preaching Benefits the Preacher

There’s a bizarre, schoolmarmy undertone in the rants of the SoV proponents. Like, what do they care what we all do with our bitcoin? If SoVs and MoEs necessarily overlap, why lecture everyone that bitcoin is ackchyually a SoV exclusively? Nobody’s hindering their preferred use, so what gives?

Remember the US dollar? The USA convinced the world to go long on the USD. If you convince the world to hoard what you’ve already started hoarding, then you’re in a very good position. You’re stoking demand for what you can supply.

But you don’t even have to supply it. Convincing others to covet your hoard lets you borrow against it, giving you access to leverage. If your hoard grants you these benefits, it can trade at a multiple. If you have n bitcoins in your hoard, you might be able to sell shares of your hoard at a 3n valuation. You’ve just figured out how to push the inflation rate of a deflationary asset up to 300%. Dastardly, but clever.

The beauty of freedom money, though, is that no one can tell you how to use it. Sure, I’m telling you it’s underestimated as a MoE, and I have a vested interest in its use as a MoE, but I’m not telling anyone what to do. I’m describing what I see and debunking some bad, possibly disingenuous claims.

Store your bitcoin where and how you want, spend it where and how you want, and its value depends on what we all do collectively, no what some suits do in their exclusionary conclave. Nor does it depend on what some talking head on twitter said is best. Of course, when the majority of the world’s freedom money is held by a select few, then it won’t be very free.

Bitcoin is flexible enough for all our diverse needs, and we all have a say in what it is and what it will yet become. Let our diversity be our strength.

This is a guest post by Roy Sheinfeld. Opinions expressed are entirely their own and do not necessarily reflect those of BTC Inc or Bitcoin Magazine.

{kind=link}